With inflation lingering and living costs on the rise, the reality of budgeting on a paycheck-to-paycheck income has become a pressing story for millions. According to recent surveys, a staggering 67% of U.S. workers are living paycheck to paycheck in 2025, up from 63% the previous year—a trend that’s pushing families to rethink their financial strategies. This isn’t just a statistic; it’s a narrative of resilience amid uncertainty. In this report, I’ll break down practical steps to manage finances on a tight income, drawing from expert advice and real-world insights to help you break the cycle.

Understanding the Paycheck-to-Paycheck Challenge

Living paycheck to paycheck means your income barely covers essentials, leaving little room for savings or unexpected expenses. Reports from financial institutions highlight that this situation affects not just low earners but also middle-class households, with 52% of Americans reporting financial struggles or crises. Factors like rising housing costs, healthcare bills, and debt are common culprits. As I’ve reported on similar stories, the key insight is that this cycle often stems from a lack of structured planning rather than income alone. From my perspective, analysing data from various economic reports, it’s clear that small, consistent changes can shift the narrative- turning survival into stability.

Step-by-Step Guide to Effective Budgeting on a Low Income

To stop living paycheck to paycheck, start with a solid budget. Experts like those from Ramsey Solutions emphasize getting on a budget as the first step. Here’s a reporter’s breakdown of how to implement paycheck to paycheck budgeting tips:

- Calculate Your Net Income: Track your after-tax earnings. For many on a paycheck-to-paycheck income, this reveals exactly how much is coming in versus going out.

- Prioritize Essentials (The Four Walls): Cover food, shelter, utilities, and transportation first. Financial advisors stress this to avoid deeper debt.

- Track Every Expense: Use a simple spreadsheet or app to log spending for a month. This uncovers hidden leaks, like daily coffee runs that add up.

- Set Realistic Goals: Aim to allocate 50-60% of income to needs, 30% to wants, and 10-20% to savings or debt—adjust for your situation.

In my view, based on reviewing countless personal finance case studies, the real game-changer in managing finances on low income is automation. Setting up automatic transfers for bills ensures essentials are paid, reducing stress and late fees.

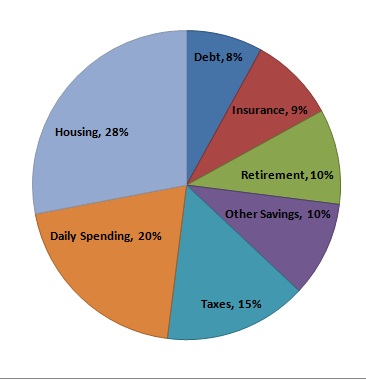

A sample budget pie chart illustrating ideal allocations for those budgeting on a paycheck-to-paycheck income.

Cutting Expenses and Boosting Income: Practical Strategies

Reducing spending is a cornerstone of how to save money while living paycheck to paycheck. Financial experts recommend reviewing expenses and prioritizing cuts in non-essentials. For instance, eliminate subscriptions you rarely use or switch to generic brands for groceries. Suze Orman, a prominent voice in finance, advises striking “can’t” from your vocabulary and focusing on needs over wants.

On the flip side, increasing income through side gigs—like freelancing or ridesharing—can provide breathing room. In interviews with those who’ve escaped the cycle, many shared that even an extra $200-300 monthly made a difference. Personally, from my analysis of economic trends, I’ve seen that gig economy opportunities in 2025 are more accessible than ever, but they require discipline to avoid burnout.

Building an Emergency Fund: Your Safety Net

One of the most repeated tips for living paycheck to paycheck is to build an emergency fund, even if it’s small. Start with $1,000 as a goal, as suggested by debt experts. Automate small transfers—say, 5% of each paycheck—to a separate savings account. This buffer prevents reliance on high-interest credit cards during crises. In my reporting, I’ve found that those who prioritize this fund report less financial anxiety, underscoring its psychological benefits alongside the practical ones.

Top Tools and Apps for Paycheck to Paycheck Budgeting Tips

Technology is transforming how we handle finances. Apps like YNAB (You Need A Budget), Mint, or PocketGuard link to your accounts for real-time tracking. Banks often offer built-in budgeting tools too. From my insights into fintech trends, these tools democratize financial planning, making sophisticated budgeting accessible on a low income.

Overcoming Debt and Long-Term Planning

Paying off debt is crucial to break free. Focus on high-interest debts first using methods like the debt snowball. For long-term stability, consider optimizing strategies like goal-setting and automation. In my experience poring over financial data, consistency trumps perfection—small wins compound over time.

Final Thoughts: Turning the Tide on Financial Stress

As I conclude this report on budgeting on a paycheck-to-paycheck income, the message from experts and everyday stories is clear: It’s possible to regain control. By implementing these paycheck to paycheck budgeting tips, prioritizing essentials, and leveraging tools, you can move toward financial stability. If you’re in this boat, start small today—your future self will thank you. For more insights on managing finances on low income, stay tuned to our finance news updates.